Using Medicaid Annuities to qualify for Medicaid Benefits

What are Medicaid Qualified Annuities

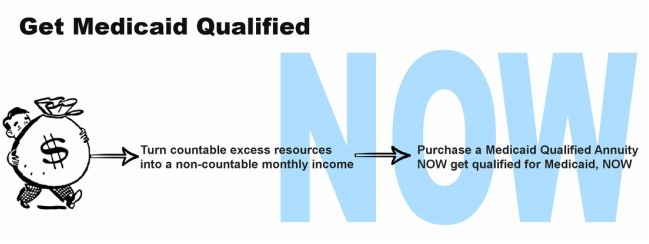

Medicaid Qualified Annuities are an essential tool for Medicaid planning, they take excess countable resources and convert them to a stream of income.

They are funded with a single payment, they begin paying a monthly income immediately and they are structured to meet the guidelines set by the Deficit Reduction Act of 2005 section 6012. They are available only through a select few insurance companies and are generally used as Individual and Community Spouse Medicaid Qualified Annuities.

What is the DRA [Deficit Reduction Act]

The Deficit Reduction Act was signed on Feb. 08, 2006 and part of the DRA established new guidelines for Medicaid, including the eligibility criteria. Section 6012 particularly refers to the evaluation and treatment of Annuities as related to eligibility. It states that in order to not be treated as a transfer, they must meet certain guidelines.

We provide attorneys and individuals with the knowledge and guarantee that our annuities meet all of the requirements set by the DRA [Deficit Reduction Act] of 2005 Section 6012 as stated below:

- The annuity is irrevocable and non-assignable

- The annuity is actuarially sound [payment schedule does not exceed the annuitants life expectancy]

- The annuity provides payments in approximately equal amounts, with no deferred or balloon payments.

- The State Agency must be named as the remainder beneficiary a. under the DRA the annuity must name the state as the beneficiary in the first position [they will recoup from this the total amount of Medicaid benefits paid]. Unless there is a community spouse and/or a minor or disabled child. b. If there is a community spouse and/or a minor or disabled child, the state may be named in the 2nd position, after those individuals.

How do the annuities work;

Medicaid Annuities are purchased when someone is either in or about to enter a nursing home and needs to qualify for Medicaid but has resources and assets in excess of the allowable limits set by Medicaid. The annuity is funded using the excess resources, therefore protecting them from the "spend down" process. They immediately begin paying an income either to the community spouse or the individual, turning “countable assets” into “non-countable” streams of income. The individual will then qualify financially for Medicaid either reducing or completely eliminating the high costs of nursing home bills.

What are the benefits of a Medicaid Qualified Annuity?

1. Qualifying for Medicaid will immediately reduce or eliminate the high cost nursing home care.

2. Convert excess countable resources to a non-countable income stream for the community spouse, accomplishing 2 goals;

a. Preserve assets and prevent them from being used for the high cost of nursing home care.

b. Prevent the community spouse from having insufficient income to pay for daily needs and expenses.

3. A single individual can convert excess resources and use the income to fund their nursing home costs at a reduced Medicaid rate [up to 55% less than private pay] and potentially pass along the excess to their beneficiaries.

4. A single individual can also use an annuity to pay nursing home costs during a penalty period incurred after "gifting" a portion of their excess resources to a family member to shelter assets.

4. Asset protection. The annuity will protect assets and allow you to pass them to a community spouse or family member.

Examples - click to see examples of how someone can preserve assets, transfer wealth, reduce nursing home costs and create a stream of income for the community spouse with a Medicaid Qualified Annuity

Our Medicaid experts will help guide you through the process of purchasing a Medicaid Qualified Annuity and/or an Irrevocable Funeral Expense Trust and get your clients Medicaid qualified fast

Questions?

Call us Today 855.471.6771

For expert Medicaid Planning and Medicaid application assistance contact Medicaid Plus, P.C www.mymedicaid plus.com